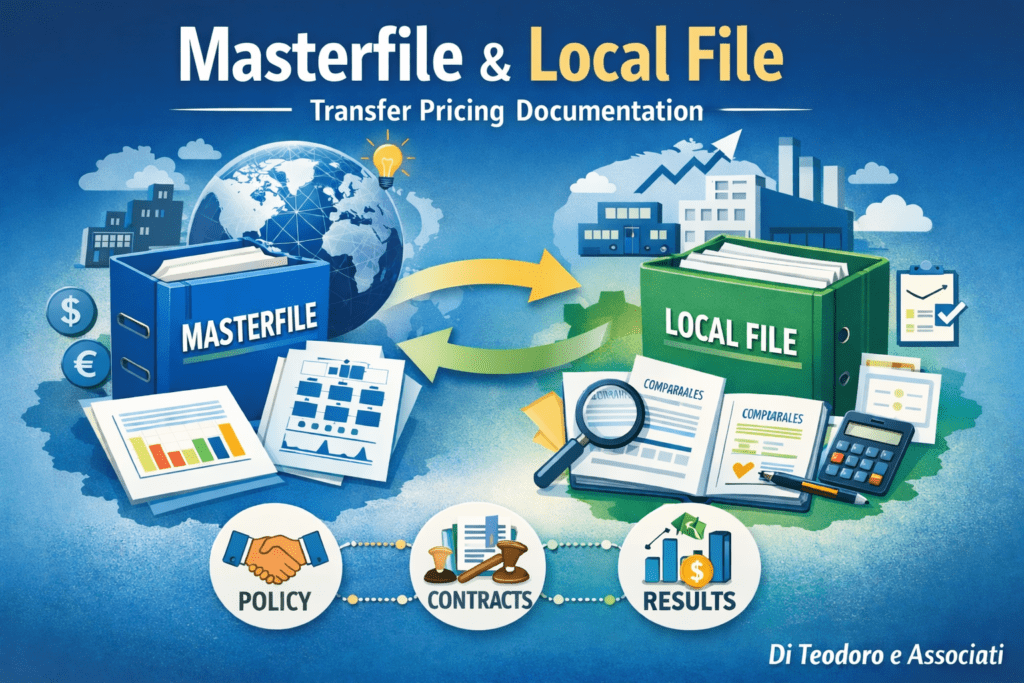

Masterfile and Local File: TP documentation as a verifiable narrative.

In transfer pricing, documentation is not a marginal compliance requirement attached to the tax return: it is where a group makes the link between its business model and its intercompany results understandable—and therefore auditable. This is why the Masterfile and the Local File work only if they are treated as two levels of the same narrative: one explains the group’s logic, the other shows how that logic takes shape in the country.

The framework originates from the BEPS Action 13 approach: Master file, Local file and, where required, the Country-by-Country Report. In Italy, for penalty protection purposes, the operational cornerstone remains the combination of the Masterfile and the National Documentation (the ‘local file’ in practical terms). The differentiator is less the number of pages and more internal consistency: what the group states at the ‘high’ level must be reflected in the local transaction, in the contracts, and in the numbers.

The Masterfile is the map: the group’s structure, value chain, intangibles, financial and pricing policies, and decision-making processes. This is where it is defined who creates value, where capabilities and risks sit, and who governs the intangibles. A useful Masterfile is not marketing; it is a document that enables the reader to understand why, for example, a local entity performs routine rather than strategic functions, or why it bears certain costs and not others.

The Local file is the evidence: it lists and characterizes the Italian entity’s material intercompany transactions, reconstructs the functional analysis, selects the method, documents the economic analysis, and reconciles the TP perimeter with the accounting data. This is where the frictions that most often trigger challenges come to the surface: functional labels that do not match reality (a ‘limited risk’ entity that actually sets prices and discounts), intra-group services with no evidence of benefit, royalties described as remuneration for intangibles that are not managed in a consistent way, and comparables reused without an updated rationale.

The critical point is the linkage. A dossier can be formally correct and, at the same time, fragile: it only takes the Masterfile and the Local file telling two slightly different versions of the same group. Consistency is not an editorial matter; it is a governance matter: who approves the policy, who implements it, how it translates into margins, how year-end adjustments are managed, and which internal controls ensure that contracts and actual operations align.

From this perspective, the Masterfile and the Local file also become a management tool: they force the group to write down the ‘official version’ of the operating model and to verify whether the numbers support it. When this becomes a continuous process, documentation stops being an event and becomes a standing control.

Daniele Di Teodoro

managing partner